Music x Web3: Why direct engagement between artists and fans can create more value for their co-owned community

Napster destroyed everyone in the music industry. Spotify-led streaming brought the industry back to growth but in a way that gave artists even less power. Web3 can help them take it back.

As I mentioned in my initial post (link), there’s a ton of hype in Web3. With asset volatility out of control, the crypto naysayers are waiting for everything to crash and burn. When I initially came up with the idea for this newsletter, crypto was flying high. We’re now in another “crypto winter”. Crypto bear markets are the perfect time to build, and that’s exactly what I plan to do with this newsletter. Over the coming months, I’ll be focused on putting out more and more content on a regular basis starting with the exciting world of music.

The Music NFT scene is a microcosm of the Web3 space. Hype everywhere. We have a ton of Web3 people feeling super bullish about blockchain disrupting the current state and removing middlemen. On the flip side, you have naysayers pushing back saying that this is all hype with little transformative value. To cut through surface level discussions, let’s briefly cover the history and current state of the music industry and then discuss ways in which Web3 can transform the paradigm and create more value for artists, fans, and the community they can create and own together.

History: Convoluted copyright laws based on outdated distribution models

Music is a cultural universal and has forever been a source of entertainment across all forms of humanity. As society and economic markets matured, music (like most industries) required frameworks and laws to provide clarity on ownership and economic value generation. Unfortunately, the music legal landscape is notoriously complex. The copyright laws and legal framework that govern the music industry were created during a different era with different distribution and business models. As we think about future business models and potential disruption, it’s critical that we ground ourselves in these laws and how they impact incentives.

Copyright laws grant ownership for “original works of authorship” and were created with the stated purpose to promote art and culture. These are the laws that assign a set of exclusive rights to authors, including how they make and sell copies of their works, create derivative works, and perform or display their works publicly. There are two types of copyright laws for music specifically: 1) composition copyright and 2) master recording copyright. Composition Copyright covers the written lyrics, notes, and melodies for any given song or album. This is typically owned by the songwriter through the publisher. Master Recording Copyright covers the literal recording of the underlying composition and music. Think of this as the actual recording from the studio that eventually gets pushed to Spotify or Apple Music (or back in the day to vinyl records or CDs). This is traditionally owned by the three major record labels.

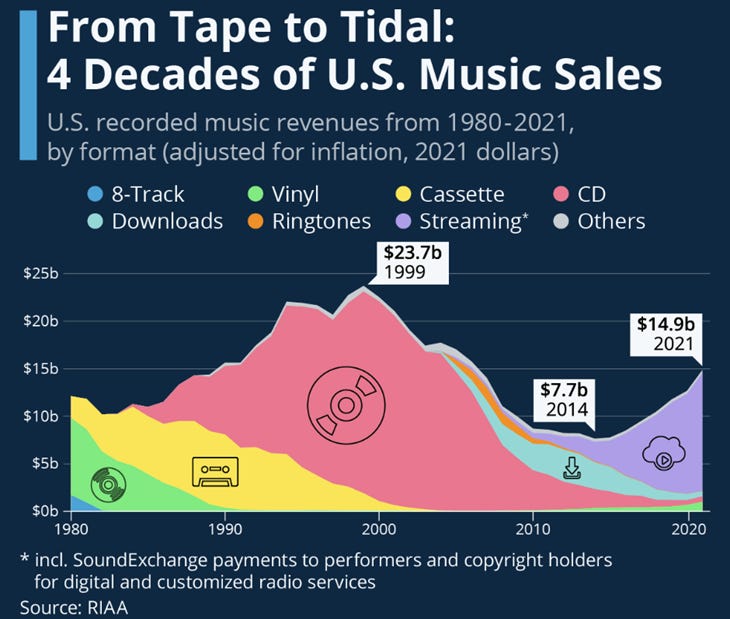

These copyright laws were established here in the U.S. as part of the Copyright Act of 1976. With this in mind, let’s look back at the evolution of distribution models over the past 50+ years. The graph below is very informative as we look at revenue and which formats dominate financial value generation.

When these copyright laws were enacted, vinyl records were the dominant format of music with cassettes just starting to enter the scene (making up just 6% of total revenue). From 1976 until 2000, we had amazing technology innovation that enabled transition from vinyl records to cassettes to CDs. With this came all sorts of innovation with how fans consumed music. We had Sony’s walkman and discmans (no skip please!) and music enabled vehicles with 5-disc changers. While this innovation was incredible, the distribution model largely stayed the same. Major label records took the following approach: 1) sign emerging artists with a strong following, 2) create and produce music in a studio, 3) market it on the radio, and 4) sell and distribute the crap out of the physical version of it (no matter the format). Combine that with lucrative tours and merch and everyone is fat and happy. For all my millenials out there, here’s a pic of a Sam Goody to bring back some nostalgia of going to grab the new release.

Due to the relationships with all key stakeholders across the industry and the capital needed to get studio time, produce content, and run the engine to push out physical albums, recording labels quickly became powerful players in the space. This leverage enabled them to negotiate favorable contracts with artists who needed their backing to make it in the space. As this took shape, the norms around value capture solidified. Music labels put up a large upfront investment in return for the rights to royalties through the master recording copyright mentioned above. Importantly, the terms on these deals were extremely favorable for labels. We’re talking 75-80% of future royalty revenue. Moreover, in these deals, the artist has to recoup this investment before they can make any money. This clip from Financial Times is pretty informative, but it’s clear and obvious to everyone now that labels maintain a ton of power and with that comes lucrative rents. There’s all sorts of nuances with the copyrights and how money is distributed, but the most critical aspect is who gets access to the master copyright which is where the majority of revenue comes from. As the industry matures, we also start to see consolidation which further strengthens the power of labels. All of that being said, all parties across the space (artists, radio stations, labels, etc.) were feeling good about the 1,090% growth from 1990-2000… until two college kids in a dorm blew sh*t up.

Disruption and evolution to the current state: From Napster to Streaming Wars

In the summer of 1999, Sean Parker and Shawn Fanning launched their peer-to-peer file sharing service which would change the industry and consumer expectations forever. With the internet hitting mass adoption, Napster enabled users to share digital files with anyone they wanted. While other companies were doing something similar, Napster had a strong emphasis on mp3 files and music. Fans soon had the ability to download and share music for FREE. They could then burn the songs onto a blank CD/CD-RW and have whatever music they wanted for a long road trip. Pretty sweet for them… terrible for artists. Music was being leaked before releases. Sales took a massive hit. Everyone from artists to labels to retailers got crushed.

While everyone was getting crushed, Napster was flying high and raised a $15M Series C round in May 2000. At its peak, Napster had more than 20 million users using the service. Things were great for Sean and Shawn… until the lawsuits rolled in. Apparently enabling the infringement of copyright laws wasn’t cool. Napster was up for just under 2 years then was abruptly shut down by the legal authorities.

Did Napster ever make any money? I was actually trying to remember if I ever saw ads back in the day. I did some googling and found this gem on boards.straightdope.com. The internet back in 2001 sounds so fun :). P.S. - does this feel like a Discord chat to anyone?!

With Napster getting abruptly shut down, this paved the way for emerging tech companies to capitalize on the demand for owning and listening to digital music.

Apple

Napster completely changed consumer expectations and paved the path for Apple’s iTunes and the streaming we know today. In 2003, Apple launched the iTunes store in conjunction with the big, bulky iPod that we all used to know and love. This enabled users to buy a song for $.99 and albums for a price similar to that of CDs. Napster alone destroyed a lot of value for the industry (just look at the chart above from 1998 to the mid 2000’s). Apple’s move created a world where you could own digital versions of individual songs or albums as long as you stayed within their walled off Apple garden.

With Napster being shut down and Apple charging a buck to own a song, radio once again became the main source for music fans to discover new music. This model gives artists the ability to market their music and for fans to explore songs without having to own them. While passionate fans had a desire to own their digital music, there was so much free music already flowing across the web that the momentum around consumer expectations (free or close to free music) was so strong. With the internet revolution in full-swing, we quickly had the rise of internet-native radio apps.

Streaming

Pandora was launched in 2000 initially as a B2B company that would license the “Music Genome Project” to retailers based on its recommendation system. Given the shifts in the music industry, it pretty rapidly shifted to a B2C internet radio app with a freemium model. This was extremely easy to monetize via ads. Rather than listen to the local radio stations, users were now able to search any artist or song and play a station that played that song and other songs you might like based on the recommendation system. Searching for and saving songs and artists enabled a more personalized experience than your local Z100.3. After initially launching as a freemium model with ads, Pandora quickly realized it could offer a subscription fee to users who wanted to listen ad-free.

All of this innovation came before iPhones and the shift to smart, mobile phones. The release of the iPhone in 2007 would drive further innovation in the space. Rather than being tied to a computer to listen to your streaming service, you could eventually listen to music on the go wherever you are. This paved the path for Spotify and the dominance it maintains today. Today, Spotify maintains roughly 30% market share and is the clear leader among your favorite tech companies (Apple, Google/YouTube, Amazon) and Pandora (owned by SiriusXM). The experience that Spotify and others offer today to its users is pretty amazing. However, it’s worth understanding how the streaming and Web2 flywheel works for music today and what problems this presents for the people actually creating our content – artists.

Problem to be solved: How Web2’s music flywheel works and what’s broken

Spotify generates revenue via two channels: 1) advertisements (ads) and 2) subscriptions (subs). Streaming music platforms are focused on maximizing # of users and overall time spent on the platform so they maximize revenue across both revenue channels. In order to optimize ad revenue, they combine their robust music library with their ability to manage and analyze all user data to enable better ad targeting. More subscribers and optimized ad revenue give Spotify more cash to create and acquire content which reduces the cost of paying licensing fees to labels and artists. All of this can create an even more advantageous economic situation which can be leveraged to acquire more users which feeds the whole flywheel. Let’s look at how this impacts the various stakeholders involved.

The artists are clearly not making out well in this set-up. It’s crazy that the bands, teams, and individuals that are actually making the content we are willing to pay for are by far the worst off in this environment. To put this in perspective, here’s an interesting fact about the streaming music economics:

For an artist to make a minimum wage in New York City ($15/hour or $32,000/year), they would need 13.2 million streams on Spotify

Putting all of this history and the current state together, let’s lay out the specific problems that need to be solved

Current streaming economics exacerbate the uneven balance making it hard for artists to compete and make a living: Artists today still view labels as the gatekeepers to their success. The “big 3” labels have benefited greatly by the streaming business model which has further strengthened their position. All the revenue generated from subs and ads goes into a single pot which is then dispersed based on the total number of streams. This means that if Taylor Swift accounted for 10% of streams, she gets 10% of the revenue from this single pot. Given Spotify has a lot of power in terms of how they create playlists and algorithmically tee up songs to users, this creates opportunity for the bigger labels and artists to maximize the value they are extracting while making it extremely hard for niche and emerging artists to compete. This is great for established players but makes it harder and harder for niche and/or emerging artists to make a living.

Artists are incentivized to become an attractive investment for labels rather than delivering value to fans willing to pay for their creations: Artists know how much power labels and the big streaming platforms have in the current model. Because of this, they are incentivized to serve their needs rather than support their community of fans. This means doing whatever they can do to build a following on TikTok and driving up metrics on other social platforms to make the case for a big contract. Can these things build community and support fans? Sure, but I think we have a lot of artists playing this game rather than supporting and engaging their passionate fans.

Fans have no way of financially benefiting from the upside if they support an artist or song early on before they “make it”: Due to the other challenges and limitations to date, fans have no mechanism to benefit from the upside if they find an artist early before they go mainstream. While they can pay for music, attend shows, buy merch, etc., they don’t have any ability to financially benefit from their willingness to support artists in the early days.

Enter Web3: The power of community and co-ownership between artists and fans

With large platforms dominating the space and extracting a large portion of the value, blockchain and decentralization offer an opportunity to disrupt the status quo and shape a new engagement model between artists and fans. Web3 allows for more rapid and robust engagement between creators and those willing to pay for artistic creations. Flywheels are an important framework to use as we consider new possibilities. After thinking through the current state of music and listening to a16z’s crypto school lecture on crypto business models, I shaped a new flywheel that can emerge in the world of Web3 music. Before we get to specific players and how the space is evolving, let’s review this framework and what it means for the future.

In this new world, we start with artists and creators creating amazing content. Investors (some of whom may be fans) then have the opportunity to invest in the content by way of owning the digital assets. Prior to blockchain, proving digital ownership of any asset (e.g., picture, song, etc.) as you moved across the internet was not feasible. Yes, you could buy a song on iTunes for $0.99, but you did not have the ability to do anything with that song outside the Apple ecosystem of products. The Web2 tech platform model was built to acquire users and monetize their time spent on the platform. The shift to Web3 is all about ownership and will enable users to engage across platforms and companies in a way that wasn’t possible before. Artists are already “dropping” their music in the form of NFTs and “limited digital assets” which provides a new source of revenue and investment needed to build their business. This leads us to platforms. Given our ability to leverage ownership of a token across platforms, this opens up our options. While there could be brand new platforms that emerge that are native to Web3 (these are currently being built), we can also leverage the Spotify’s of the world. Smart contracts enable us to establish terms for royalty, second party sales, etc. that were not possible in the previous world of tech. Platforms’ ability to integrate and leverage music NFTs and smart contracts will move us away from a world where every stream costs the same amount of money and the other problems mentioned above. The possibilities get a whole lot more interesting. This leads to third party developers and other ventures.

Composability is another hot topic and buzz word getting thrown around the space right now. What is it? Composability within blockchain gives us the ability to freely use and integrate code from other applications into their products. Think of this like lego blocks – mix and match to put pieces together and make magic. Worth checking out this post from Packy. Once investing and owning in music digital assets is established and functional platforms exist, this gives us the ability to open up a whole new world of music experiences. Exclusive access to shows and experiences for super fans who own particular assets. Free merch for NFT owners. Private IRL and digital events that connect artists directly with their fans. This isn’t pie in the sky thinking – it’s already happening today!

This leads us to the last and most critical part of the flywheel – the community formed by direct engagement between fans and artists. In the current and historical model in music, artists were forced to work directly with labels if they were going to make it big or even make a modest living. Labels then influenced how artists grew their content and brand. Many passionate music fans call this “selling out”. The community and culture that forms around this new engagement model can create more value and utility for both artists and fats. Fans can invest in artists they love while enjoying the upside if this investment results in more success for the artists. They can also help shape how the community and culture grows over time (think DAOs for those closer to the space). Moreover, artists are able to get investment from super fans in a way that wasn’t possible before. Artists also get to engage directly with fans to understand what resonates and how they can best support the community. Power and control now shifts from label companies in the middle to the individuals, teams, and communities creating and enjoying music and additional ventures and experiences created.

Let’s consider some of these dynamics with my girl Taylor in mind. Those who know me well, know I’m a huge T-Swift fan. Yes, a Marine that loves Taylor (there’s actually a ton of us!). I’ve been a huge fan since her country days (I actually wish we did more country still!). This acquired podcast from Acquired on her story is amazing and worth checking out. What was interesting here is how Taylor knew early on how important it was to engage directly with fans. Taylor has 27,000 interactions with fans on Tumblr over the years. Here’s a quote from her first major album:

"I love everyone who has inspired me to write a song whether you know it or not. I love anyone who has ever turned the volume up when my song comes on the radio. Anyone who has bought this album, anyone who can sing along to my songs when I play them live, anyone who's ever requested my song on the radio, or even remembered my name, if you ever see me in public, I want to meet you. I will thank you myself. You have let me into your life and I will never be able to thank you enough for that. I love you. I love God for putting you in my life."

This strategy clearly worked wonders for Taylor and was a huge part of her early success as an artist. However, what’s unfortunate about this situation is that the early fans that created this wave, built community, and funded this start were not able to benefit from any of this upside. Changing this will be the magic that propels Web3 music forward. Let’s envision how this could play out for a new upcoming Taylor-like artist in the future. Let’s call him/her SWIFTYv2...

SWIFTYv2 records music and starts to share with a few early supports and collaborators

SWIFTYv2 plans a unique NFT drop to potential fans that includes a VR experience with the artist and fellow supporters. As part of the drop, fans can purchase/invest in the album or song via an NFT

Funds from the NFT drop give artist capital to build a brand, record and distribute music, and build a small team

Owning the NFT gives fans the ability to join a virtual community on Discord (or some better, web3 version of it)

Fans, community members, and SWIFTYv2 now have a space where they can shape the future of the music and culture together (maybe even form a SWIFTY DAO?)

As part of owning the NFTs, owners also benefit financially from streaming revenue as the song is played on Spotify (and others) and also have exclusive access to experiences with the artists and other fans (private meet-ups on tour, merch, etc.)

As the artist creates more content, the community brings more people into the space making the NFTs for existing and future albums even more value which provides more capital to keep building this out

This energy and investment propels the community forward and results in tremendous upside for both artists AND fans – BOOM!

P.S. – The success of one community now propels others looking for the next artist who will make it big (basically the same thing we’re seeing play out today with NFTs as everyone looks for the next BAYC, but this time there’s actual utility in way of royalty revenue, access to artists, etc.)

Current Players in the Space

For those newer to the space, you might be there thinking… yea, cool dude but this is all pie in the sky thinking. Not gonna happen. I’m here to tell you that this is happening… TODAY! There are players across the space (disruptive start-ups and established incumbents) that are already starting to shape the future model. This cuts across the entire landscape – streaming, NFTs, royalty models, major labels, artists (new and old), and others. Here’s a very high-level (and not exhaustive!) list of some of the key players today in the space.

Established players are waking up to this new reality

If all of this didn’t make you believe that this is real, let’s quickly discuss recent news from major players in the music industry.

Warner Music x OpenSea

Warner Music Group (one of the three major music labels) recently announced a partnership with OpenSea (the largest NFT marketplace). In the announcement, Warner announced that the partnership will allow their artists “would get early access to OpenSea’s new drops product, along with improved discoverability, personalized storytelling on customized landing pages, and OpenSea’s industry-leading safety and security features”. They also have their own dedicated drop page to host limited-edition projects, which would open new opportunities for fans to engage with music and artists”. The new engagement model between artists and fans is real and going to blow up.

Spotify Hunting for Web3 Talent

A few months back, it was reported that Spotify was on the hunt for Web3 talent in a strong signal that music NFTs will be part of the future. This shouldn’t come as a surprise, given that Spotify acquired Mediachain labs (blockchain start-up) back in 2017! It’s not clear exactly how the space will take shape, but it’s clear that this isn’t going away and new business opportunities will appear for both new and established players.

Innovation can seem to happen gradually then all at once. While people tend to attribute innovation to big moments where “X new idea/start-up/model came out of nowhere”, there’s typically progress, small steps, failures, small successes that occur over an extended period of time that result in the big moments that have a massive impact on the future. I believe that music right now is on the verge of having its moment that awakens people up to Web3. While this is extremely exciting for music and the artists and fans that bring this space to life, it’s just as exciting to bring more excitement to additional opportunities in the Web3 space overall.

Closing Thoughts

If you made it here, THANK YOU for reading. I hope you enjoyed it as much as I enjoyed researching and organizing my thoughts. The future is very exciting, but increasingly hard to predict and understand. I remain bullish that blockchain and Web3 will create positive change in the world and look forward to exploring new spaces. Music is unique in that it touches just about everyone across the world. I’m excited to see this space playout and even more excited to jump into a new area to understand how Web3 will impact our world moving forward.

Keep on keepin’ on,

Butch